Digital Wealth

How a Platform Model Can Help Wealth Managers Win

The last two decades have been a time of significant growth, change and evolution for the wealth management industry.

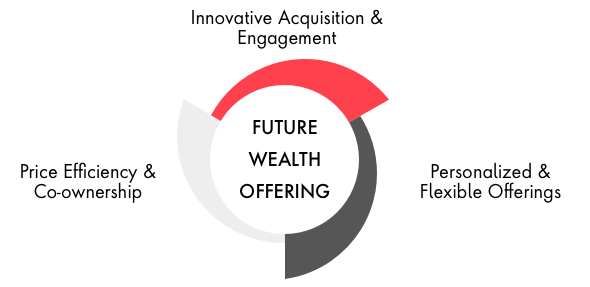

Assets under management (AUM) have quadrupled from 31 trillion to 112 trillion. The rise of robo-advisory and the trend towards a fee-based service model are transforming the industry, as is the rise of newer asset classes for alpha (alternatives, IPOs, digital asset) and investing with purpose (ESG). At the same time, customers continue to look for higher returns, holistic financial wellness support, better digital experiences and lower fees.

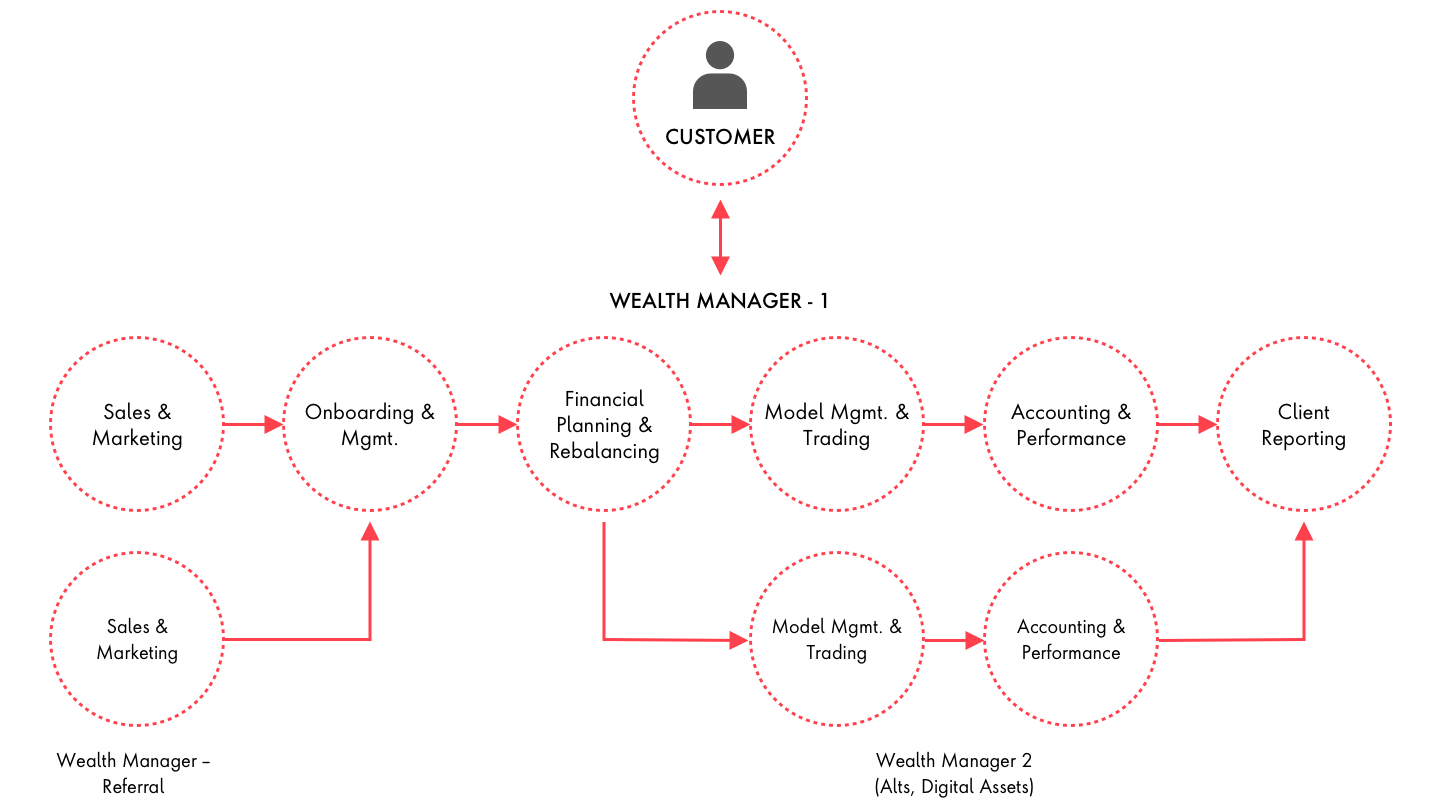

To support these changes and increase efficiency, wealth managers have structured themselves around service offerings (e.g. advisory only, full-fledged advisor, model manager), segments served (e.g. mass affluent, HNW, UHNW) and products offering (e.g. MF/ETF, EQ/FI, alts, digital).

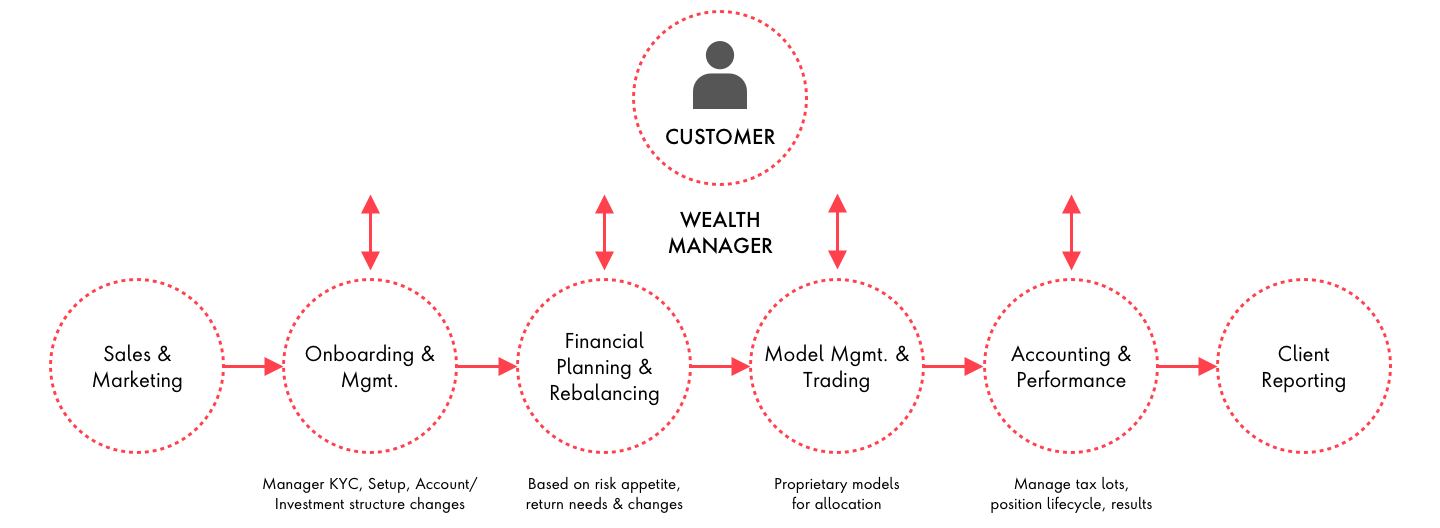

They have also organized people, process, and technology as an “assembly line”—a linear chain in which each function is tightly coupled with another.