Platform Transformation

Help Write Banking’s Next Chapter: The Promise of Platform Transformation

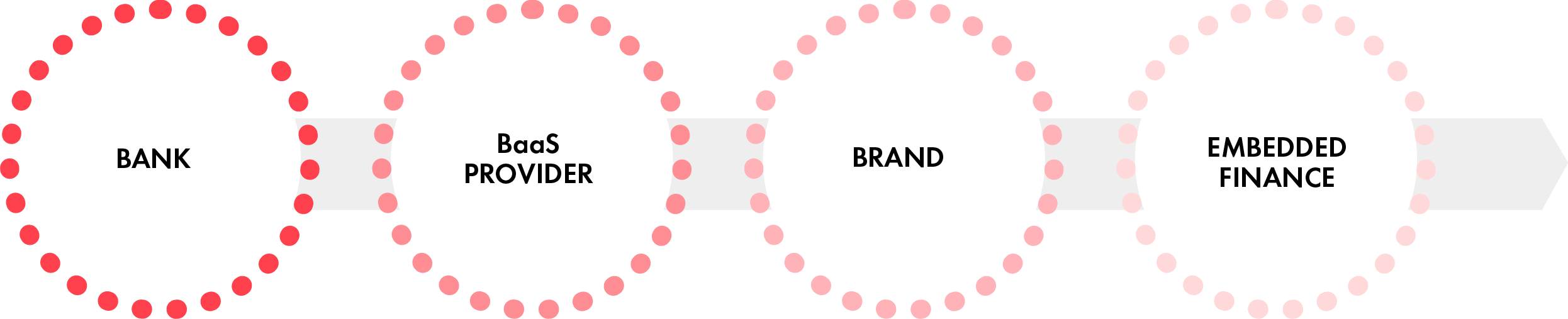

What do people need from a bank? (1) Somewhere secure to deposit their hard-earned cash, (2) the ability to move money around and (3) a way to access credit to fund major purchases and smooth out expenses between pay days. But fintechs are chipping away at all aspects of banking. Paypal (not a bank) already does the first two. Revolut (not a bank yet) does the first two and is starting to do the third.

Tech startups and other nonbanks have successfully embedded financial products into their digital offerings—chipping away at the market share incumbent banks enjoyed. Paying back a friend on Venmo using emojis isn’t just convenient and sociable. It’s participation in a seismic shift of how money is managed and transmitted: the fintech revolution.

Juniper Research expects the total number of people using digital banking to reach 3.6 billion by 2024. That’s a 54 percent increase from 2.4 billion in 2020. The past decade was marked by massive investment in fintech companies and growing profits.