Insurance

The Future of Insurance: Digital Strategies Are a Key Driver For Success

As an industry, insurance has traditionally been cautious about change. But the rapid advancement of new technologies in recent years has propelled competition from new insurance start-ups as well as from surprising industries that are using data and artificial intelligence to move into the insurance sector.

Insurers have long understood the importance of data. Actuaries base their business on using data to assess risk, policy features and costs. What has changed is the scale of data available, the way it is gathered, and the tools available to use it. Take, for example, the exponential rise of health data that is transforming insurance. Unlike in the past, data can be collected and analyzed in a matter of seconds - and it can be deployed for customers and organizations via apps and other digital systems immediately. Hence insurance companies are focusing on operating at this level of data collection, analysis, and deployment in order not to lose business and opportunities to those companies that can.

What are the external and internal challenges the insurance industry is facing in the year ahead? In some operational areas, insurance is already playing catchup - but there are opportunities traditional companies can take advantage of, and digital strategies can help capture that market share.

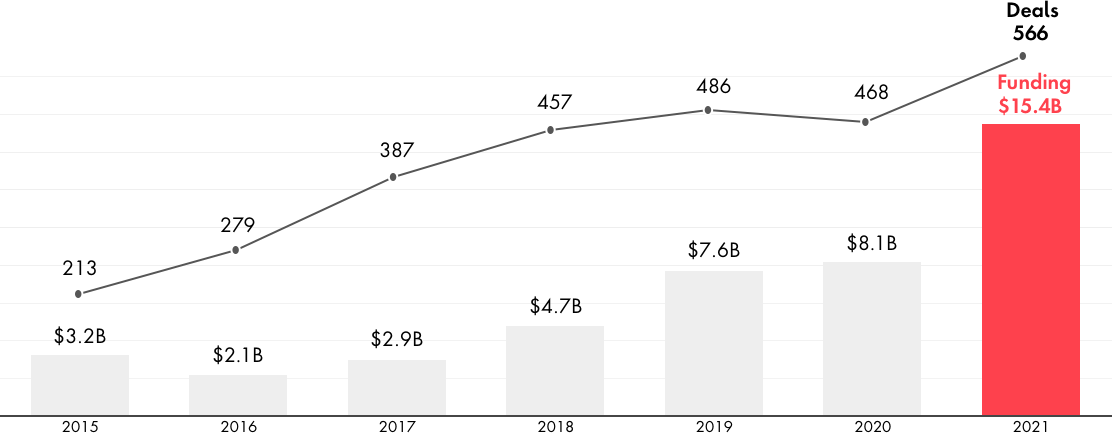

Investment in ‘insurtech’ is growing fast, jumping by 90 percent in 2021, compared to 2020, with over $15 billion in funding. With embedded insurance, usage-based insurance (UBI) and apps that create a better user experience in areas such as claims are creating disruption.